‘We must accept finite disappointment, but we must never lose infinite hope.’

Martin Luther King

Slack Investor experienced plenty of disappointment this financial year. On reflection, most of it was self induced. He was dazzled by some of the growth projections that he found on Market Screener – and forgetting that these are just analyst forecasts – and sometimes not achieved. As a result, he got involved with too many early stage companies that experienced regulatory failures – or just fell short of expectations. This year, there was also the AI scare that put the shivers up owners of software and healthcare stocks. These sectors could be vulnerable to cheaper AI interventions that might affect future incomes.

This post is just one part of the annual review of the Slack Portfolio. The percentage yearly returns quoted in this post include costs (brokerage) and dividends but, the returns are before tax. These raw figures can then be compared with other investment returns.

Slack Investor uses the incredibly useful Market Screener to analyze the financial data from each company. This excellent site allows free access (up to a daily limit) to analysts’ data. Once you register with an email address on their site, you can use the financials tab to get information for each stock.

Slack Investor uses forward-looking numbers – so, sometimes, things can go wrong. He extracted the predicted 2028 Price/Earnings (PE) Ratio and Return on Equity (ROE) and average forecast revenue growth for the financial years 2027 and 2028. He usually requires that the forecast Earnings Per Share (EPS ) growth will be greater than 15%. He then condenses all this information into one number, the Slack Ratio. This is the ratio of forecast ROE/forecast PE.

The Slack Ratio, is a way to make things easy for Slack Investor’s limited brain. This ratio is still ‘experimental’ and used to differentiate between stocks. The higher Slack Ratio, the better. Slack Investor generally likes the Slack Ratio to be above 0.7.

Slack Investor Stinkers – FY 2026

Financial year 2026 was again big on volatilty. Slack Investor knows that stinkers are a part of the game, even in good years. Unfortunately, he managed to attach himself to a multitude of stinkers this year. Slack Investor managed to be in some unfashionable sectors – and, in hindsight, also made some bad individual company selections. Again, this is just part of the game.

Botanix Pharma (BOT) -60%

(BOT – Forecast 2028: PE 3, ROE 28%, Av. Growth 30+%, Slack Ratio 9.3). Slack Investor entered the murky and volatile world of Biotechs with a small stake (0.2% of portfolio) in this Australia-based dermatology company. Their topical gel (Sofdra) is used to treat excessive underarm sweat. This has to be Slack Investor’s weirdest purchase – and he was sold on the ‘sizzle’, not the steak. The company is ‘expected’ to be profitable in 2028. However, the market has some doubts about this. Slack Investor bought on the good numbers (above) at $0.35, sold in November 2025 at $0.14. Latest price $0.02 – A humiliation!–and a lesson in getting involved with speculative stocks.

CSL (CSL) -50%

(CSL – Forecast 2028: PE 12, ROE 18%, Av. Growth 30+%, Slack Ratio 1.5). CSL is a big holding for Slack Investor (6.3 % of portfolio). CSL was a Stinker in FY 2025, but they have continued to spend on Research & Product Development at levels around 10% of revenue. This should be a good thing for future earnings. However, a series of earnings downgrades and management changes have tested market confidence in the company. Slack Investor realizes that CSL is not the growth machine that it once was – but it still is one of the world’s leading biotechnology companies. At this stage, he is sticking with CSL and is buoyed by some recent price rises –but he feels that his loyalty has not been rewarded and would have no problems in selling his stake if a better opportunity presented.

REA Group (REA) -41%

(REA – Forecast 2028: PE 24, ROE 33%, Av. Growth 15+%, Slack Ratio 1.3). This real estate powerhouse has been part of the Slack Portfolio for a long time and it too might be losing its mojo as a growth superstar. Property is cyclic in nature and this FY there has been a softening in property listings and therefore revenue. The market quickly bailed out. Slack Investor has the long view on this one. Future numbers (above) still look reasonable and he is prepared to ride this one out.

Telix Pharmaceutical (TLX) -38%

(TLX – Forecast 2028: PE 32, ROE 9%, Av. Growth 30+%, Slack Factor 0.3). This company develops and markets radio-pharmaceutical products that are used to treat cancers in a precise fashion. TLX is less than 1% of the Slack portfolio and is his most speculative stock as the company is not predicted to be profitable till 2027. FY 2026 has been tough on Telix with some regulatory hurdles and some other trouble with US authorities. These problems seem to be mosly overcome and the share price has risen – but there is still some risk. The ROE is low, but the projected growth is over 100%. If the positive momentum continues, Slack Investor will add to his position.

Cochlear (COH) -35%

(COH – Forecast 2028: PE 20, ROE 18%, Av. Growth 25%, Slack Ratio 0.9). COH is a great Australian company but it has had a shocker of a year with a series of earnings downgrades. In a counter-cyclic move, Slack Investor bought 5 months ago at about $190 after the first downgrade announcement. Mistake! These downgrades seem to usually occur in bunches. At the current price of $120, it seems good value. Will stick with this one and try to learn from this error.

Wisetech Global (WTC) -34%

(WTC – Forecast 2028: PE 18, ROE 17%, Av. Growth 30+%, Slack Ratio 0.9). WTC has great logistics software that is the industry standard. The underlying business is solid and was unfairly dumped during the AI scare. However, the real problems have been with the scandals associated with the founder and executive chairman Richard White. Mr White has recently resigned and this has triggered a share price recovery. The recovery is going well and Slack Investor is considering adding to his share parcel in WTC.

Slack Investor also went backwards with many of his other holdings. Car Group (CAR) -29%; Technology One (TNE) -27%, though it was a nugget last FY +124%; Plenti Group (PLT) -24% – What was Slack Investor thinking?

Slack Investor Nuggets – FY 2026

Nuggets are a blessing in any portfolio. Fortunately, this Financial Year, there were some bewdies! Slack Investor continues to invest in high Return on Equity (ROE) companies with a track record of increasing earnings. If expectations are met, companies with these qualities sometimes behave as ‘golden nuggets’.

Codan (CDA) +122%

(CDA – Forecast 2028: PE 32, ROE 28%, Av. Growth 15%, Slack Ratio 0.9). Codan is a technology company that specializes in communications and metal detecting. What a great company – also a nugget in FY 2025(+75%)! It is one of Slack Investor’s core holdings. CDA has had a checkered past – a nugget in FY 2021 (+161%), a stinker in FY 2022 (-58%), a nugget in 2024 (+54%), and again a nugget (+75%) in 2025. What has kept me in the stock was its low debt, (generally) increasing earnings, and the high profitability (ROE 28%).

SKS Technologies (SKS) +73%

(SKS – Forecast 2028: PE 15, ROE 63%, Av. Growth 30+%, Slack Ratio 4.2). A recent purchase, SKS is an electrical and networking service company that delivers ‘advanced technology solutions’. It has recently landed big contracts for data centres and has a further upstream tender pipeline of $1.25B AUD. These ‘contract for income’ companies need constant surveillance but Slack Investor was at a Wilson Asset Management seminar this year and a speaker impressed him with his ‘Picks and Shovels’ approach to investing in the new wave of AI and Large Language Models (LLM’s) … and he did, and would like to buy more!

RPM Global Holdings (RPM) +71%

(RPM – Forecast 2027: PE 154, ROE 53%, Av. Growth 38%, Slack Factor 13). RPM is a mining services provider that had a happy association with Slack Investor. There was a takeover early this year by the NYSE-listed big company – Caterpillar. Slack Investor had to bow out – but with money in his pocket!

Alphabet (GOOGL:NASDAQ) +36%

(GOOGL– Forecast 2028: PE 20, ROE 22%, Av. Growth 25%, Slack Ratio 1.1). What a powerhouse. Alphabet continues to have high profitability (ROE 22%). There are some concerns over reduced earnings in 2027, AI spend, and competition – but his everywhere company keeps surging ahead. Happy Owner.

Vanguard Asia (Ex-Japan) ETF (VAE) +30%

(VAE – Market Screener Data unavailable. VAE is one of Slack Investor’s core holdings – providing exposure to Asian Markets. After a lacklustre few years, it has finally started to provide the growth from Asia that Slack Investor envisaged. A Long-term hold.

Some honourable mentions to some top results this year that didn’t quite make the nuggets. Megaport (MP1)+27% and Coles (COL) +19%. COL is now, not in the Slack Portfolio, but in his Stable Income portfolio.

July 2026 – end of Month Update

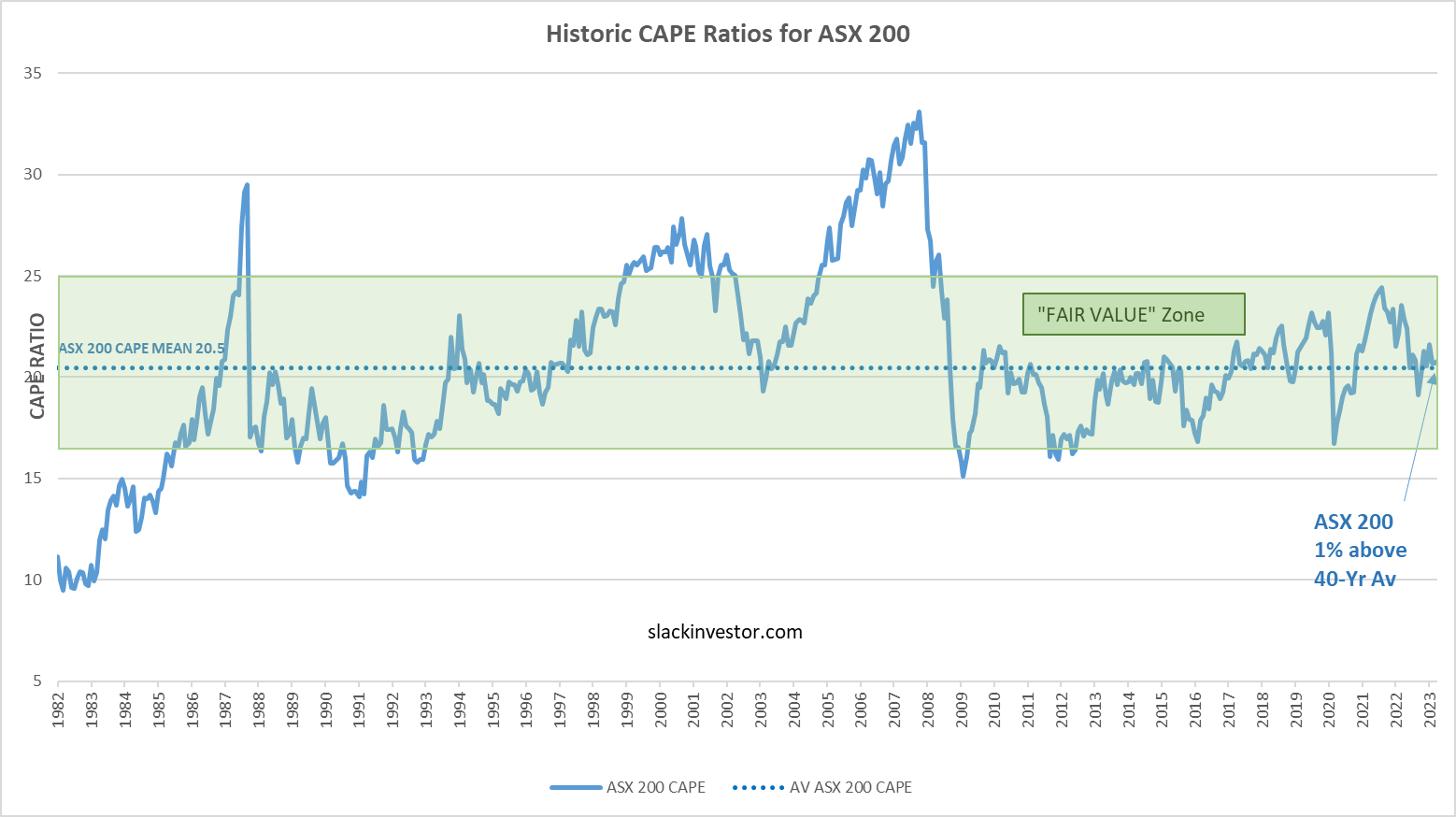

The new financial year has started off positively for the Australian and UK markets. The ASX 200 +2.3%; FTSE 100 +3.5%. The S&P 500 is taking a well-earned breather and has had a flat month (-0.1%). He remains IN for all index positions.

All Index pages (ASX Index, UK Index, US Index) and charts have been updated to reflect the monthly changes.

{kind=link}

{kind=link}