Slack Investor has a healthy regard for those who make a living based upon their performance. It is a general financial wisdom that, if you are following large companies, you will very probably be better off in the long term with passive index funds.

However, some active boutique stock pickers may have an advantage when it comes to smaller international companies. In this category, 33.65% of active funds are able to outperform over a 15-yr period.

Slack Investor is currently backing his own abilities on the stock picking front. But, there will come a time when I lack the ability or inclination to do the (admittedly limited) research work. Also, there are some Slack Investor readers who would like to outsource this task.

Hyperion Global Growth Companies Fund ETF (ASX: HYGG)

I don’t follow individual companies in overseas markets that closely – but there are those that do – and do it very well.

Hyperion are Brisbane-based and started this managed fund back in 2014. They have also offered access as a listed ETF on the ASX since 2021. The ETF would be the way that I would buy it.

HYGG is not a low-cost fund as it has a Management Expense Ratio of 0.70% and an outperformance fee of 20% against benchmarks. The ETF, to date, has not paid a dividend. However, in this case, it seems that the managers are offering good value net of fees.

One-year performance (2024 May +47.3%) is impressive. However, Slack Investor is after the real grafters who can produce impressive results over the long-term. Hyperion is establishing a case for consideration.

The advantage of an active fund manager is that they can be nimble and take advantage of any opportunities that the Hyperion analysts discover.

| Holdings | % Portfolio Weight | 1-Year Return | Forward P/E |

|---|---|---|---|

| Tesla Inc | 12.29 | 65.9 | 166.67 |

| ServiceNow Inc | 9.42 | 34.16 | 60.98 |

| Microsoft Corp | 7.95 | 10.73 | 33.11 |

| Palantir Technologies Inc Ordinary Shares – Class A | 7.65 | 498.55 | 263.16 |

| ASML Holding NV ADR | 7.15 | -20.81 | 28.74 |

| Spotify Technology SA | 7.1 | 143.26 | 71.43 |

| Amazon.com Inc | 7 | 12.14 | 33.67 |

| Block Inc Class A | 5.72 | 2.88 | 17.73 |

| Meta Platforms Inc Class A | 4.61 | 41.9 | 28.65 |

Table of the top holdings of HYGG, their portfolio weight, 1-yr return, and forward PE at May 2025.

When it is time to really ‘get on the couch’, Slack Investor would take a look at these blokes to invest his money. This Hyperion crowd seem to know what they are doing.

June 2025 – End of Month Update

The financial year closes and the Australian, UK and US markets are all in positive territory for the financial year.

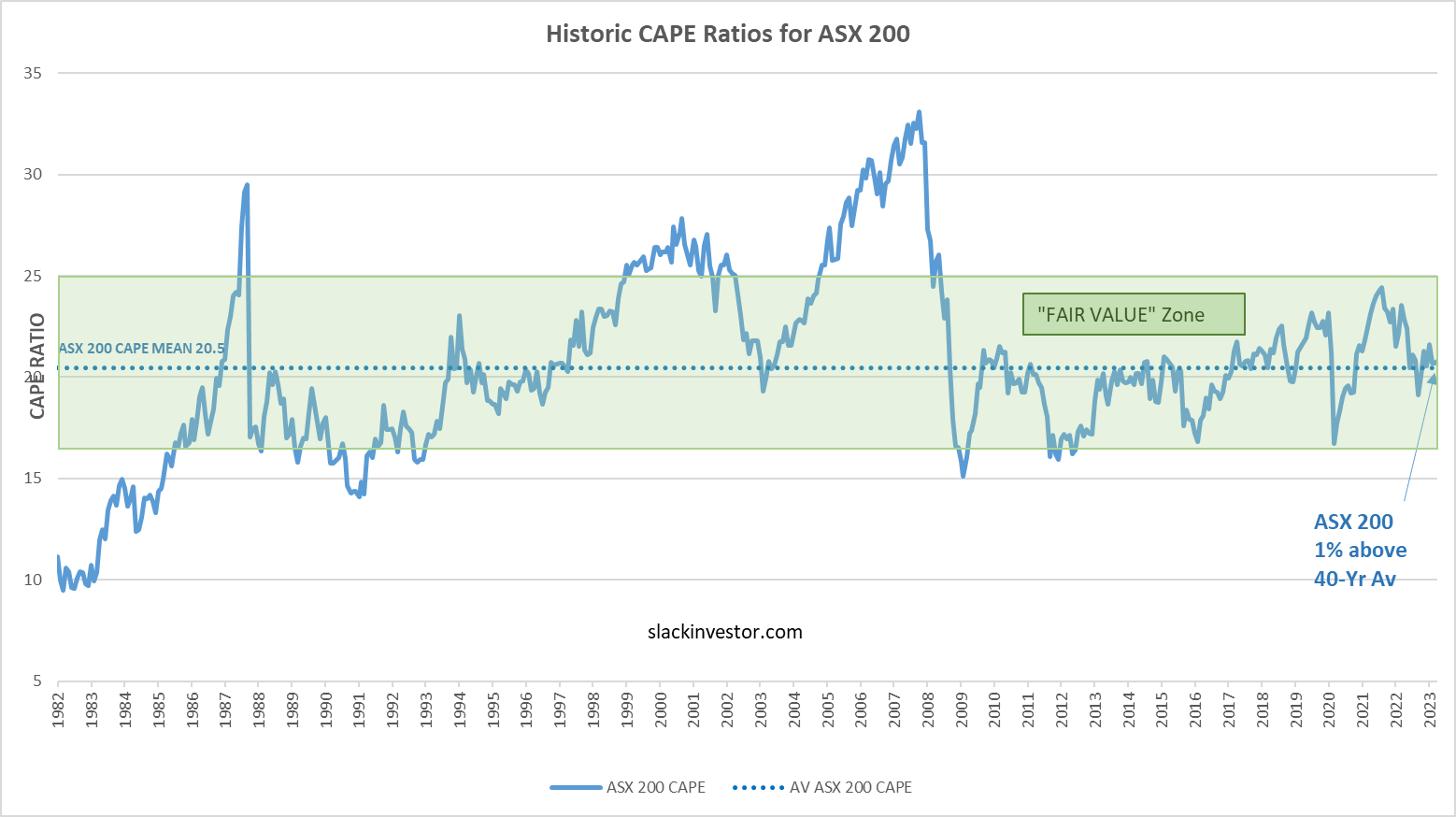

Slack Investor remains IN for all followed markets. The ASX 200 (+1.3%) and FTSE 100 (-0.1%) moved modestly. It is a continuation of good times in the US with the S&P 500 rising 5.0%. Are our American friends delusional in an expensive US market? Or, is Slack Investor missing something.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index). The quarterly updates to the Slack Portfolio have also been completed.

{kind=link}