Slack Investor remains IN for US, UK, and Australian index shares.

Slack Investor remains IN for US, UK, and Australian index shares.

The Slack Investor has been true to his ethos and not published any general interest posts for a month … this will happen from time to time … but I will commit to prompt monthly updates for those who follow the US, UK and Australian indexes and who may value the Slack input to their buy/sell decisions – these will be published in the first couple of days of each month.

I have been off to New Zealand. The great advantage of the Slack approach to investing is that I can be away from the markets – even out of internet range for up to a month at a time – the lack of required decisions on a daily, or weekly, basis suits my style.

New Zealand is a remarkable country to which Australia is the older, louder, uglier, more arrogant brother! I had a great time and the the Kiwis would often impress with their manners, integrity and general genuineness(?).

We were mostly in the South Island and the scenery was jaw-droppingly beautiful. … I want to go back! Slack Investor and travelling companions are shown casting appropriately shadowy figures on Day 3 of the Milford Track – Nice photography skills from my sister-in law … Enough of the travelogue.

March 2017 has seen rises, in the UK and Australian markets and a refreshing pause with the US Index. It is also dividend season down under and Slack Investor always enjoys this time when each company (hopefully) shows their appreciation for supporting them with a little trickle into the bank accounts.

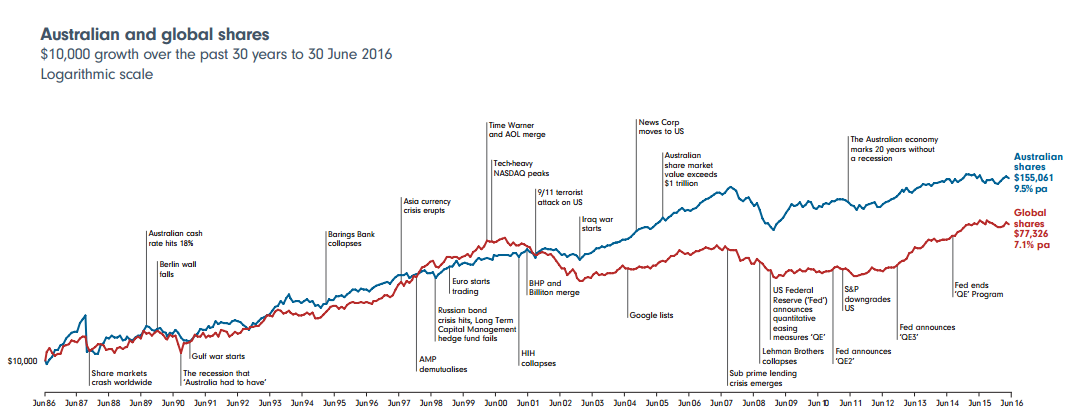

For more information on parameters such as progressive gains, look on the Slack investor ASX Index, US Index and UK Index pages for updated details – and a look at the charts. I have also updated my Portfolio page – this portfolio page will only be updated occasionally and is not presented as an investment guide – it just shows the type of companies that Slack investor is interested in – mostly growth companies with established dividend records. Next end of month update on the index charts will be early in May.

{kind=link}