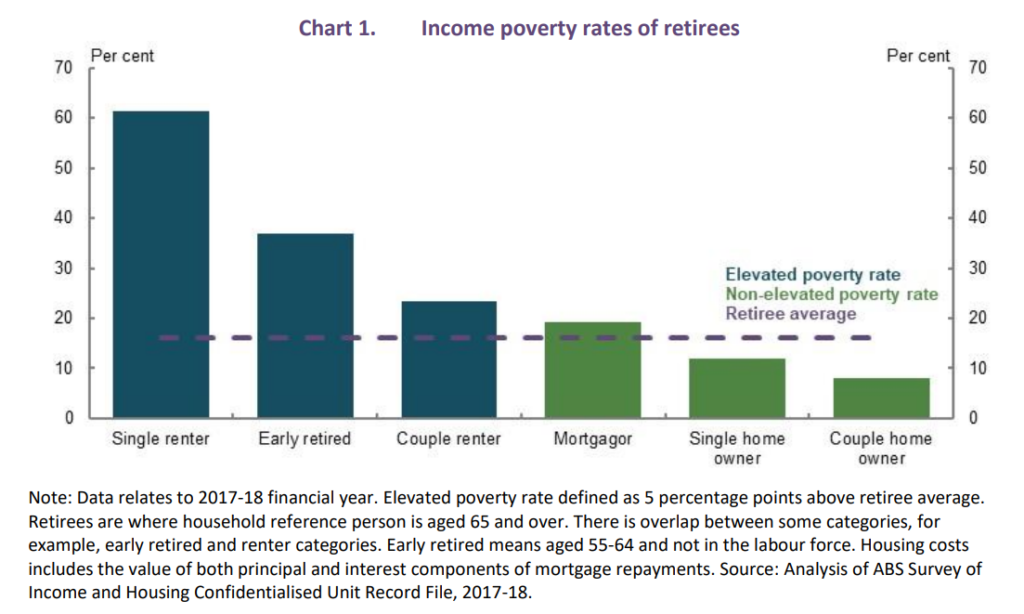

After discussing how hard it is for those trying to buy their first home. Slack Investor is compelled to provide some hope in the desire to own your home before you retire. The numbers are in … and, not owning a house in retirement or, losing your job before you retire, puts you at real risk of not reaching a comfortable financial position.

Whereas very few retired home owners are in poverty, most retired renters are …

There are very few existing incentives on the dusty twisted road to home ownership. They include Stamp Duty exemptions/concessions that vary from state to state. In Victoria, they are available for homes less than $750K. There is also the First Home Buyers Grant (FHBG), which, again, is dependent on which state you live. In Victoria, that comes in at a measly (but I’ll take it!) $10K.

All of these things are worth considering and applying for when you finally purchase a home, but the First Home Super Saver Scheme (FHSSS) is a lesser known arrangement that seems to make sense – but it requires a bit of “setting up”.

In order to make the most of the FHSSS, you’ll need to start planning well ahead of the time to buying a house/apartment (3 – 4 years?) – But planning ahead is the very trait that Slack Investor loves!

First Home Super Saver Scheme (FHSSS)

I did refer to the First Home Super Saver Scheme (FHSSS) way back in 2017 when it was just a twinkle in ScoMo’s eye – it started as an election promise to get the “young folk” on board as the government felt a need to at least be seen to be doing something to help first homeowners.

These voluntary contributions can be withdrawn from your super when you finally ready to purchase a home – by filling out an ATO form for a ‘determination’. The determination will tell you exactly how much you can withdraw – it will be a little more than you have put in (your contributions – up to $50K – plus deemed earnings)- and waiting a month.

Getting the money out usually takes 15–25 business days … once you withdraw money to buy a house, you have one year to use it

These extra contributions are over and above the compulsory super that your employer makes. The scheme works by making an arrangement with your paymaster to salary sacrifice into your super – up to $15K per tax year. Contributions can also be made by arranging with your super provider to make a personal super contribution.

The tax savings come about as, you only pay 15% tax on these super contributions – rather than your marginal rate of say, 32.5%. Plug in your own details into this calculator to determine your possible tax savings.

I would recommend all prospective home owners to take a look at this scheme. Assessment for eligibility is made on an individual basis … so couples and friends can combine their amounts – but start now – it will take a few years to get a useful house deposit.

Colonial First State outline a case study of a couple that have each started voluntary extra super contributions of $15K – After 15% tax this comes down to $12 750 p.a of contributions into their funds. After 4 years, they each have amassed $55K (4 x $12 750 plus deemed interest). A combined house deposit of $110K was possible using the FHSSS – and, using a favourite Slack Investor way of saving – deductions from your salary before you even see it! All of this with tax advantages.

Homework (get it!): – Potential homeowners – read about it – and get on the FHSSS!

Even Superman has his limits – Is it Kryptonite OR Brussell Sprouts?

Slack Investor writes a lot about Superannuation because it is a fantastic component to have in your armoury to establish financial independence – in a tax-effective way.

The ultimate aim for Slack Investor is to fund your own retirement, but in reality, according to the Association of Superannuation Funds of Australia (ASFA) estimates, a minority (43% ) of Australians of retirement age would be self-funded by 2023 – this percentage should increase as the compulsory superannuation system matures.

Before we get to this mix, by the time you retire, you do want to have a place to live and be free of landlords. This may sound impossible to some at the moment – but it is a vital part of financial independence. It can be a “tiny home”, an apartment, a place in a regional area …. as long as it is yours!

Tiny Homes – This 20 sq m little bewdy will set you back $32 000 – however, you still have to find land for it – and connect to services.

It is so important to aim to own your own home by the time that you retire – even if it is a 1-br apartment. Admittedly, this is so much harder than it used to be! Looking at the figures below, it is vital to get as large a home deposit as you can to reduce your borrow amount – this should be one of your early financial goals. However, without help, a multi-bedroom home near a capital city now seems near impossible.

If you dont have a deposit, October 2023 data showed that Australians need an income of more than $300,000 a year to buy a median priced home. Household incomes required were considerably less, but still “eye watering”, for outer suburbs and regional cities. e.g. Geelong $243,333, Brisbane $223,333. Apartments are usually less expensive – and require less income to service the home loan.

At its most basic level, superannuation is forced retirement savings for all working Australians. A compulsory contribution of 11.5% of your salary (from 1 July 2024) that will compound till your preservation age (between 55 and 60).

According to Treasury projections, about 60% of retirees will have less than $250 000 in super in 2024. This amount of super is not enough to fund a comfortable retirement. $250 000 in pension mode at the official Age 67 drawdown rate of 5% generates only $12 500 income per year. Clearly, many Australians will need to rely on a mix of their super and the aged pension for retirement income. The Aged Pension is available to Australians over 67 – but, it is means tested.

The bare minimum to aim for is the “sweet spot” in the aged pension asset test where your assets are a bit more than the maximum allowed for the full pension. Under current rules (2024), home owning couples can have $451 500 in assets (singles $301 750) and still qualify for the full government aged pension (at age 67).

In 2020, the Alliance for a Fairer Retirement System pointed to a super sweet spot of around $400,000, which can see a pensioner (home-owning) couple “earning $1,000 a month more than a couple with $800,000 in savings.”

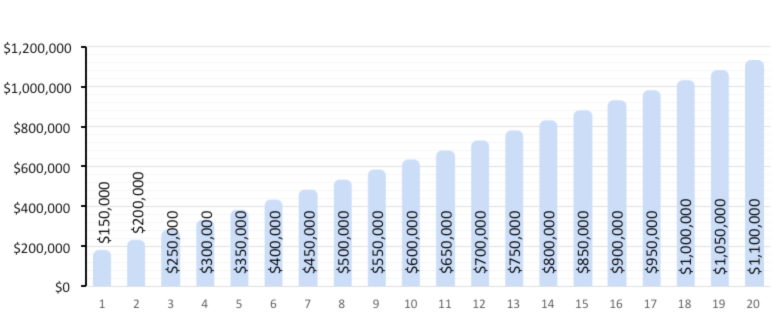

The first chart shows 20 different amounts of superannuation that you might have saved up by the time you are ready to retire – ranging from $150 000 to $1 100 000 above chart – from saveoursuper.org.au.

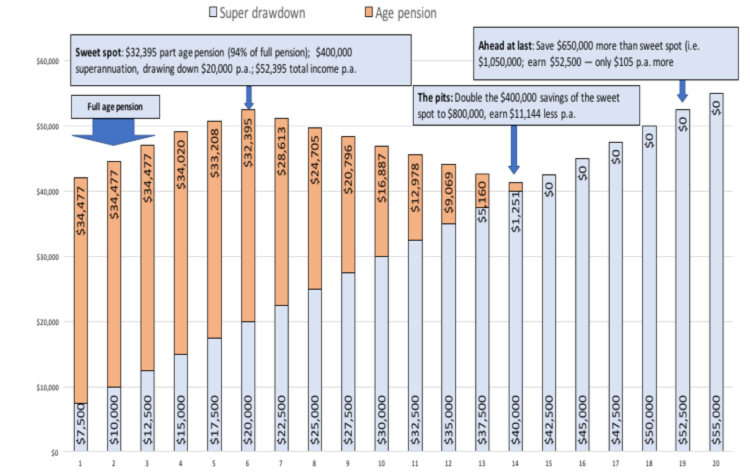

This next chart is far more interesting, it shows your total income from different amounts of superannuation (shown in the above table) mixed with the aged pension – for a home owning couple. For simplicity, these tables assume your only non-home assets are in super and the aged pension rates were those applicable in 2021 ($34 777 per couple). The essence of the table is still valid.

Total amount of retirement income – for a home owning couple – Combination of Part-Aged Pension (orange) and 5% of Superannuation Balance (Blue) for each of the 20 amounts of Superannuation Balance shown in the first chart (Using data for 2020/21)- saveoursuper.org.au

Bizarrely, there is a point on the total retirement-income (couple) table corresponding to around $400 000 in assets/super where an increased assets/super balance does not lead to an increased total income due to the asset test pension taper rate. Above that point, for those on the part-pension/super mix, the more super you have, your total income actually goes down. This strange anomaly exists for assets/super between $400 000 and $800 000 (2021/2020 data).

Clearly, the current assets test to qualify for the aged pension is unfair and provides a disincentive to save -and should be changed. But, until then, a major retirement goal is to use your super to get your total assets to near the sweet spot before you reach age 67.

(It)is not fair that people who forgo consumption and save more to increase their living standards in retirement and reduce their reliance on an Age Pension should instead get less retirement income. This is the perverse outcome for a large range of savings under the 2017 assets test.

How the Assets test works (in real life) for the aged pension (2024 Data)

According to Services Australia, for the aged pension, assets are property or items you or your partner own in full or part – this does not include your home! It does include Financial Investments (Bank accounts, shares, managed funds, annuities, etc), Personal assets (Home contents and vehicles), Superannuation and Real Estate.

I had a recent example of filling in an assets form for a close relative. Her bank statements and investments were easy to quantify. We were advised that personal assets should be valued according to what we could get if we were “keen sellers”. It was suggested to us that, other than vehicles, most peoples personal effects would amount to between $5000 and $10 000. This proved to be near the mark as most furniture and home items end up having to be donated when finalizing a deceased estate.

For the table below, the aged pension and asset limits are current values* and correct at February 2024. Using 2024 data, the “sweet spot” for assets is now near $451 500 for couples ($301 750 for singles). If you had $250 000 in super, and your “other assets” added up $60 000 (Car $13 000, Bank Ac’ts/Shares/Funds $35 000, Home Contents $12 000). Your Total assets would be $310 000.

For a couple with similar “other assets” and a combined super of $400 000, your total assets would be $460 000.

Situation

Asset Limit

Other Assets*

Super

Drawdown from Super@ 5%

Age Pension

Total Income

Single Home-owner

$301 750

$60 000

$250 000

$12 500

$28 514

$41 014

Couple Home-owner (Combined)

$451 500

$60 000

$400 000

$20 000

$42 988

$62 988

Table based on a single home-owner with $310 000 total assets ($60K + $250K) and a couple home-owners with $460 000 total assets ($60K + $400K) – using Feb 2024 values for the Aged Pension and Asset Limits.

Using this mix of super and the pension, when reaching the pension qualifying age , a modest to comfortable retirement is possible under current rules when you own your own home. Also, under the Work Bonus Rules, singles can earn up to $5304 (Couples $9360) in a part-time job without affecting their aged pension.

Comfortable lifestyle (p. a.)

Modest lifestyle (p. a.)

Couple $71,723

Couple $46,620

Single $50981

Single $32,417

ASFA calculated annual retirement requirements for those aged 65-84 (September quarter 2023) for both “comfortable” and “modest” lifestyles

February 2024 – End of Month Update

Slack Investor is IN for Australian index shares, the US Index S&P 500 and the FTSE 100.

Little movement this month for the ASX200 (+0.2%) – but, it is testing new all-time highs. Nothing happening with the FTSE 100 (0.0%) at the moment.

The S&P 500 (+5.2) and the NASDAQ 100 are hitting new record highs and Slack Investor is pleased to go with the momentum but remains nervous for these markets.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

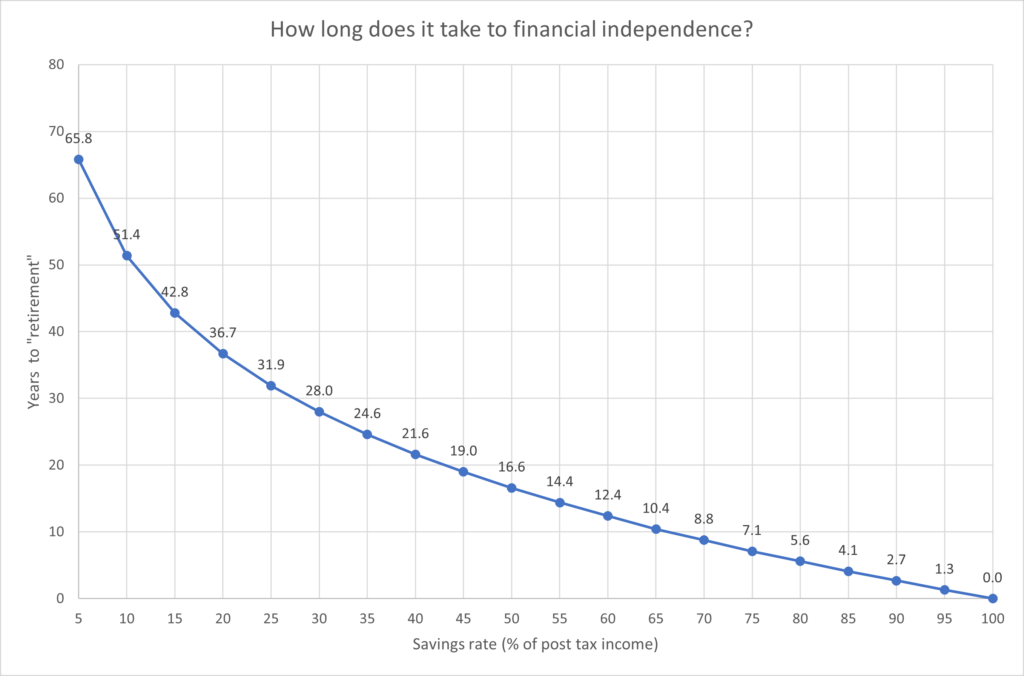

My last post on “Salary Sacrifice” got me thinking on the other things that I did to help myself on the journey towards financial independence. I have before stressed the importance of your savings rate as the primary tool in the box – and, more than anything, this is the number that will affect when you become financially independent.

This figure can be calculated a few ways, but for simplicity, let’s define it as your retirement savings as a percentage of your take-home pay (disposable income after taxes and deductions) – this can be calculated using fortnightly, monthly, or yearly data.You can work out your own savings rate or, if you are in a stable relationship with a combined goal, include your partner’s savings and take-home pay.

SAVINGS RATE (%) = 100 x (Total amount of Savings put aside for Retirement/Take-home Pay)

This savings rate is the percentage of your after tax income that you must be putting towards retirement – and it defines the number of years that you have to work until you can sustainably generate your expenses from your investments. There are some assumptions for the following chart:

This magical curve is presented below to bring a bit of clarity to your goal. The object is to get to the stage when your annual return on investments (Passive income) cover 100% of your expenses. This represents the beautiful state of financial independence.

From The Escape Artist – using the conservative assumption of a 5% return on your retirement portfolio after inflation.

In Australia, with compulsory superannuation, 10% of your gross salary is deducted from your wages. Taxation rates will vary, but lets just say that 10% of your gross salary is the equivalent of about 15% of your net salary (disposable income). You add your superannuation to any other retirement saving that you are doing to get your total amount of savings put aside for retirement.

Starting from scratch, from the above graph, if you worked continuously, and only relied on compulsory superannuation you enter the full-time work force and you are 42.8 years away from a retirement – where your living expenses are covered by the passive income from your retirement savings. In other words, if working continuously, a 22-year old starting full-time work will have enough passive income to cover expenses when reaching the age of 64.8 – relying solely on compulsory super.

In Australia, there is also the aged pension to kick things along after age 67. Obviously, if you want to retire sooner and have a bit extra for holidays, and to allow a bit of a safety margin, and be financially independent – You will have to do some extra savings towards retirement yourself.

How are people going with their savings rate?

For Australians, the compulsory superannuation system provides a sound base for retirement savings (with a working life of 42.8 years). This doesn’t factor in the government funded aged pension – subject to a means test. Currently the pension (September 2023) is $28,514 per year for a single person – But who knows if this will still be available at present levels in the future. It is best to plan for your future without it – and then accept it as a bonus if you qualify.

Although this sounds OK, any disruption to your working life (ill health, family, education, retrenchment, etc) will be a real setback to your retirement plans – Any work breaks will require additional savings for your retirement. In the US, the “average” savings rate was between 5-10% for many years. Despite some impressive savings rates during COVID-19, in July 2023, the personal saving rate in the United States amounted to 4.1 percent.

You would have to say … this does not bode well for a satisfying retirement for the “average” US Citizen.

What was the Slack Investor Savings Rate?

Rusted on followers of this blog will recall that I had a bit of a delayed start to thinking about retirement. I had just arrived back in Australia after a 6-year working holiday overseas. I was aged 30, broke, and the only thing I knew was that I didn’t want to continue working in the field that I was trained in – high school teaching.

Clearly Slack Investor had a bit of work to do. Once I was in regular employment again, I set about getting the financial building blocks in order. Emergency fund, house deposit … and then savings for my retirement. I did this mostly using salary sacrificing into superannuation and building up my own private share portfolio.

There is nothing Slack Investor likes more than burrowing into my financial history using the excellent and free “Sunset” international release of Microsoft Money. I use the Australian Version. I have been using this software to track my finances since 1990 (33 years!)

Including superannuation contributions, my savings rate for retirement fluctuated between 20% and 45%. From the top graph, this represents a shifting rate that was equivalent to an overall retirement goal that required between 36.7 years and 19 years of working. Since “ground zero” at aged 30 and some extra education, I ended up working mostly full time for 28 years. Luckily, I had found a job as meteorologist that I really enjoyed.

This is not the “hard core” road to financial independence (i.e retire at 35, etc) – but Slack Investor thinks a reasonable compromise with the competing priorities of raising a family and buying a house.

Savings Rate is so important. Determine what your own savings rate needs to be to achieve your retirement goals – and automate your savings deductions as much as possible – and get cracking!.

December 2023 – End of Month Update

Happy Days. The year closes and, Slack Investor was definitely not naughty … a big December “Santa Rally” this month. All followed markets rose. The ASX 200 up a mighty 7.1%, the FTSE 100 up 4.0%, and the S&P 500 up 4.4%,

Slack Investor remains IN for the FTSE 100, the ASX 200, and the US Index S&P 500.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index). The quarterly updates to the Slack Portfolio have also been completed.

In the world of stock markets, a 10% decline from a previous peak is known as a “Correction”. Never a nice time … but Slack Investor recommends that you just put on the big pants and get used to these things. Corrections are just part of the landscape of investing in shares and Slack Investor has often written about them – and theneed to roll with them – if you are using stock markets to better your financial position.

On average, the (US) market declined 10% or more every 1.2 years since 1980, so you could even say corrections are common.

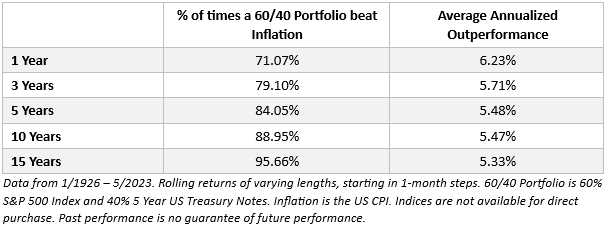

Throughout my investing career, I have been a net buyer of stocks. Selling only to raise some cash, or to shift out of one stock into a (hopefully) better performing one. Things are much the same in retirement – Though I seem to be tradingless.

I have structured my portfolio into a stable income pile and the more adventurous investment pile. My living expenses are easily covered from the dividends from the investments pile and income from the stable pile. So I never have to sell shares when their value is discounted during a correction (>10% fall) or a crash (>20% fall).

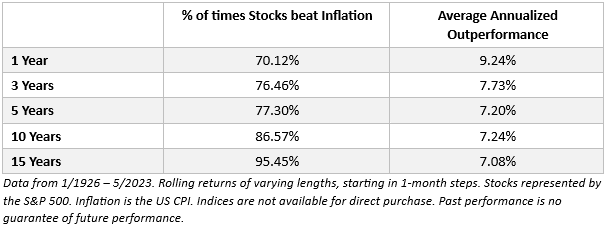

This way I can reap the benefits of long term growth in the sharemarket. The data from 97 years of following the S&P 500 Index with a balanced (60% shares:40% bonds/cash) portfolio shows that, over a 5-yr period, the portfolio will outperform inflation 84% of times by an average annual amount of 5.48%. Holding the portfolio for 15 years, it has been ahead of inflation by 5.33% on 97% of occasions. Slack Investor would take those odds.

Not for the faint hearted, but you can (historically) get an increase to returns by taking on more risk with a 100% shares portfolio. When calculated over a 15-yr period, The S&P 500 has been ahead of inflation by 7.08% (average p.a.) on 95% of occasions.

In light of the above two tables, Slack Investor shows indifference to these corrections … be patient – you will be rewarded.

October 2023 – End of Month Update

Slack Investor remains IN for the US Index S&P 500 and the FTSE 100. But is on SELL Alert for the Australian index shares – as the end of month stock price (6780) is below its monthly stop loss of 6917.

Slack investor is on SELL Alert for the ASX200 at October 31, 2023 due to a stop loss breach. I have a “soft sell” approach when I gauge that the market is not too overvalued. I will not sell against the overall trend – but monitor my index funds on a weekly basis.

Another negative month for Slack Investor followed markets (S&P 500 -2.2 %, and the FTSE 100 -3.8%, and the Australian stock market did the same (ASX 200 -3.8%).

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

The ruthless faces of the tax collectors depicted by Marinus Van Reymerswale do not ring true to Slack investor. These days, tax and fee collectors sit smugly behind desks as the fees and taxes roll in. Don’t get me wrong, Slack Investor is pleased to pay his fair share of tax … but excess fees for investing, that’s another story.

Most people have money in a super fund during their working life – this is normally known as an Accumulation Fund. When they retire, and the money can be released, they rely on this saved money to pay of debt – or fund their retirement. It is usual practice that you ask whoever runs your super fund when it is accumulating to also run your retirement fund – that pays you a pension at regular intervals.

For a fee, the super funds take care of the “back end” of this retirement fund – where your money is invested and all the administration for the fund. The Super provider sets up a new account within your super called an Account Based Pension (ABP). There is a great advantage in doing this as all earnings from from money transferred to this pension part of the fund are tax free if you are over 60. At 60, Slack Investor converted all of his accumulation funds into an Account Based Pension.

Naturally, Slack Investor is all for minimising these fees. Lets have a look at some of my favourite industry funds (Low cost high/performance) – Australian Super, Hostplus, UniSuper, and HESTA. Using the Chant West AppleCheck online tool available through the Australian Super site we can compare what they charge for running an accounts based pension.

For comparison, I invested our hypothetical ABP in the “conservative growth” option (21-40% shares) on all funds. This is usually the least risky of pre-mixed types of investments – and might be favoured by retirees. There are more other pre-mixed options that have better long-term performance – but these other options have more volatility. I have shown below the fees on a $550K account comprising of a $500 000 Account Based Pension together with a smaller $50 000 Accumulation account that you might have still running for any extra contributions.

FUND

10-yr Perf (%)

5-yr Perf (%)

Fees 500K Pension

Fees 50K Accum.

TOT Fees 550K

Australian Super

5.1

3.5

2602

322

$2924

HostPlus

4.7

2.9

3043

404

$3447

UniSuper

4.8

3.5

2696

356

$3052

HESTA

5.4

4.3

3152

362

$3514

The more you have … the more they charge.

Looking at just the cheapest of the above Industry Super providers, Australian Super with a pension account of $500K, $1m, and the current maximum amount for an accounts based pension $1.9m – again using the Chant West AppleCheck online tool.

Australian Super

Fees – Pension

Fees 50K Accum.

TOT Fees

$500K Pension Fund

2602

322

$2924

$1m Pension Fund

4802

322

$5124

$1.9m Pension Fund

8762

322

$9084

You could argue that these fees are reasonable, at around 0.5% of your invested funds, as there are inherent costs in investing and responsibly administrating these large amounts of money. Take the time to check what fees you are paying on your Super fund – and compare with a low cost/high performance fund using the AppleCheck tool – it might be time to switch funds!

Comparing Retirement fees with SMSF funds

Slack Investor is a great fan of the Self Managed Super Fund (SMSF) but recognizes that it is not for everyone – you must really be prepared to put a lot time and thought into the SMSF for it to be successful. To save on costs, rather than divesting responsibility to an accountant, Slack Investor uses a low-cost (no advice) provider and takes on a lot of the administration duties and investment responsibilities himself.

Unlike the Industry funds sliding scale for fees, a significant advantage in SMSF funds is that the costs are fixed – no matter what amount you have. For the 2023 financial year, Slack Investor’s costs through his provider eSuperfund were.

Task

Amount

Admin and Audit Costs (eSuperfund)

$1,330

Brokerage (10 trades)

$300

ETF Fees

$2,300

Time (50h@$50)

$2,500

TOTAL

$3,930

In the above example of annual fees, I have tried to include a charge for my own time at a nominal 50 hours at $50 per hour. On average, a hour per week. Most weeks I wouldn’t spend any time on my SMSF but, around tax time, and when making decisions about buying or selling, pensions, or contributions, I would spend a few hours thinking or researching. Annually, 50 hours is a fair approximation. I would gladly perform these tasks for free as finance is an interest and a hobby, but I’ve included them above to make a proper comparison – as not everyone is a Slack Investor.

Running an SMSF, because of their fixed costs makes more sense with a large super fund (>$500K). However, at the core of any successful self-managed fund (SMSF) is the amount of time and effort that the trustees (you, and other members of the fund) are willing to put into it.

Given the all the above data, it could be better, but the amount of fees that a good industry fund charges to run your pension seem reasonable at around 0.5% of funds under management. Slack Investor hopes that competition and transparency should gradually lower these fees.

September 2023 – End of Month Update

Slack Investor remains IN far all followed markets. The ASX 200 (-3.5%) and the S&P 500 (-4.9%) have had a poor month. However, the FTSE 100 is emerging from the doldrums with a positive month (+2.3%).

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index). The quarterly updates to the Slack Portfolio have also been completed.

Slack Investor has blogged about financial advice before – and although an advocate of trying to do as much as you can by researching finance world yourself, it can be a very difficult journey to be across all the fields of saving, mortgages, investment loans, insurance, superannuation, taxation, and investment.

Most people want financial advice but the problem is that it is so expensive. MoneySmart.gov.au outline a case study where “Rhett” has $400 000 to invest – He might be hit with fees of $13 600 in his first year of advice . These fees include a Statement of Advice and Insurance premiums and layers of platform and investment advice fees.

Where to invest your money is the easiest thing to sort out for yourself – with the key words being diversification and low fees. There are cost-effective ways of investing in a diversified way that will suit your risk tolerance without involving a financial advisor (e.g. Stockspot, Pearler). But some people (Not Slack Investor Readers!) need a trigger to just start investing. Finance world is much more complex than just investing your money. Slack Investor can see the need for finance professionals

Things a Financial Advisor might tell you

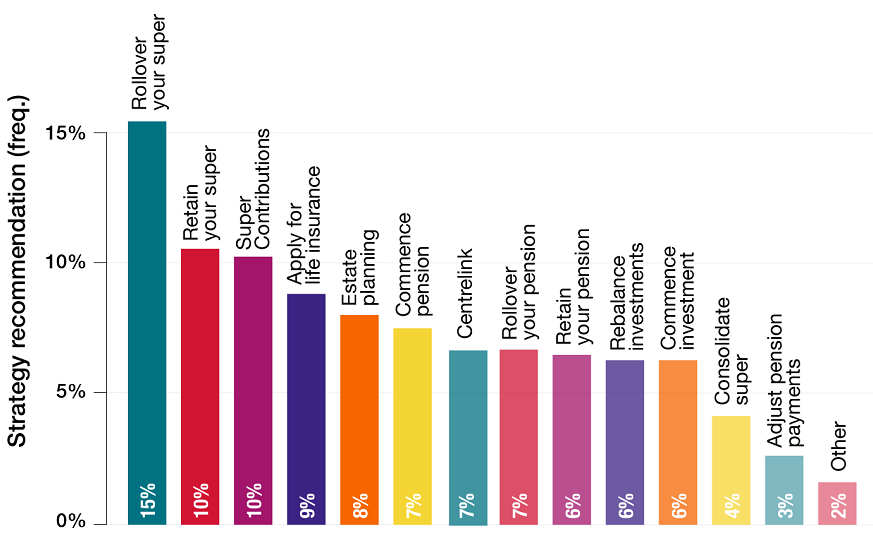

Firstlinks have trawled the data to determine the most recommended strategy used by financial advisers – the most common of these are listed below.

Let’s just have a look at some of these in more detail.

Rollover Your Super – “Rolling Over” your superannuation is just a way of describing the transfer of your “protected” super into another protected super fund. Slack Investor readers will be all over this one – Of course it makes sense to put all of your super with one provider to avoid multiple administration fees. Combine your super into one fund – preferably an industry fund (lowest fees) with a good 5-10 yr performance record.

Retain Your Super – This is again good advice for the long-term accumulators of wealth. Unless under extreme hardship, resist all attempts for early access to your super. During the COVID-19 outbreak, $4 billion was paid out to 456,000 people under the early super access scheme. This would have helped distressed businesses and individuals in the short-term but may not have been a great idea in the longer term.

Super Contributions – This is a more complicated area and, it might be good to have advice on when, and by how much ,you should boost your super contributions above those which are compulsory. This is tricky when you have competing loads on your take-home pay (Family, Mortgage, etc). Slack Investor was big on maximizing his super contributions once he had a firm grip on his home mortgage.

Apply for Insurance – When you have a family or debts (home loan?) to cover, life and disability insurance is a good idea. You don’t need an advisor to tell you this. Insurance through your super fund is usually the most cost effective way to do this.

Estate and Aged Care Planning – This area is really complicated for the layman. Professional Advice, or much research, needed.

Commence, Rollover, Retain Pension – You may need advice here if planning to mix aged-pension and super to fund retirement. If there are no aged-pension issues, Slack Investor believes that it is best to start an account pension (from your super) as soon as possible and re-contribute any surplus funds as non-concessional contributions.

Commence, Rebalance Investment – An old truth – Best time to start investing? 20 years ago. Next best time to start investing? Now! Rebalancing can be done automatically with cost-effective platforms e.g., Vanguard Super, Stockspot.

What Types of advice Do You Really Need?

The current financial advice system is complicated by well-meaning regulations that are in dire need of reform. In 2022, the Australian Treasury provided a consultation paper seeking feedback on changes to the regulatory regime that would allow financial advice on specific matters without the obligation that the advisor should know everything about your financial situation – No need for the expensive Statement of Advice (SOA).

Ideally, in a future world, you could get advice at various stages in your life from finance professionals at an hourly rate – perhaps in the same way you would consult a medical specialist about a problem. For Instance

Early/Mid-Career Advice: Am I on track with my savings, super contributions and retirement plan? What strategies should I employ to achieve my goals?

Pre-Retirement: Am I ready? Taxation Issues? Aged-pension/Super mix?

Estate and Aged Care Planning: Complicated – Many issues to discuss here.

Alternatively, you could just turn your financial future into a hobby (Like Slack Investor did), and use the internet and books to educate yourself.

May 2023 – End of Month Update

Slack Investor remains IN for Australian index shares, the US Index S&P 500 and the FTSE 100. It was a dreary month for the Slack Investor followed markets. The ASX 200 performed poorly this month – down 3.0%, and the FTSE 100 even worse – down 5.4%. The S&P 500 was flat (+0.2%) for the month.

In this month of turmoil for stock indexes, the Slack Portfolio did quite well. This is because it is heavy with technology stocks that are having a moment in the sunshine. The Nasdaq 100 index was up 7.7% for the month of May.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

A bloke with a barrow of mutilated currency circa 1910

Every quarter, the economic boffins at ASFA (Association of Superannuation Funds of Australia go to the trouble of crunching the numbers on what yearly income they think is required for a “comfortable retirement”. They assume that the retirees own their own home outright and are relatively healthy. In one year, due to inflation, the comfortable retirement amount has increased by 7.6% , or $4920, to $69,691 for a couple (Dec 2022 ).

Comfortable lifestyle (p. a.)

Modest lifestyle (p. a.)

Couple $69,691

Couple $45,106

Single $49,462

Single $31,323

ASFA calculated annual retirement requirements for those aged 65-84 (December quarter 2022) for both “comfortable” and “modest” lifestyles

ASFA’s calculations are very detailed, but notably these annual incomes do not include any overseas travel – depending on your accommodation standards and length of journey, this could easily require another $20K.

Their latest December 2022 report notes that price rises have occurred for most spending categories. In the last four quarters,

Food rose by 9.2%

Bread 13.4%

Meat and seafoods 8.2%

Milk 17.9%

Oils and fats 20.8%

Gas 17.4%

Electricity 11.7%

Household appliances 10.2%

Automotive fuel 13.2%

Domestic travel and accommodation 19.8%

International travel and accommodation 15.9%

ASFA also helpfully calculate a lump sum that you will need to supply this income – with the assumptions that the lump sum is invested (earning more than the cpi) and will be fully spent by age 92. Let’s aim high and just concentrate on the comfortable retirement – the “modest” retirement lump sum amounts are much lower (around $100K) as they assume supplementation from the aged pension.

Savings required for a comfortable retirement at age 67

Couple $690,000

Single $595,000

ASFA calculated lump sum t requirements for those aged 65-84 (December quarter 2022) for a “comfortable” lifestyle

How to Cope with Inflation

There is just one simple way – you must be invested in appreciating assets that keep pace (or exceed inflation). Appreciating assets tend to go up in value over time. This is pretty vague, but if you are unsure about an asset, try and find a price chart over a 10-yr to 20-yr period. If it is going up, it is probably an appreciating asset.

You will always need some amount in cash for day to day requirements and to ride out any investment cycles without the need to cash in your investments at a low point in the cycle.

Knowing the difference between an appreciating and a depreciating asset (e,g cars, furniture, technology equipment, boats, etc) was an important step in Slack Investor’s investing life. I can still remember the day my father gave me “the talk”, that it was OK to borrow money for appreciating assets – I think he was pushing me in the direction of real estate at the time. However, I was not to borrow for a depreciation one i.e. a car, or consumer goods – assets that lose value when you walk out of the shop!

Appreciating Assets

Below is a (not exhaustive) list of appreciating assets. I have left out cryptocurrency deliberately as it has only been traded since 2010, and it is not established yet that it is a long-term appreciating asset.

List of appreciating assets:

Real estate

Real estate investment trust (REIT)

Stocks (Shares) and ETF’s

Bonds

Commodities and Precious Metals

Private Equity

Term Deposits and Savings Accounts

Collectibles e.g. Art

Term deposits and savings accounts might keep pace with inflation (if your lucky!) – but generally do not grow faster than inflation. Slack investor will write about why owning your own home and investing in Stocks (Shares) and ETF’s are his favourite appreciating assets in a later post.

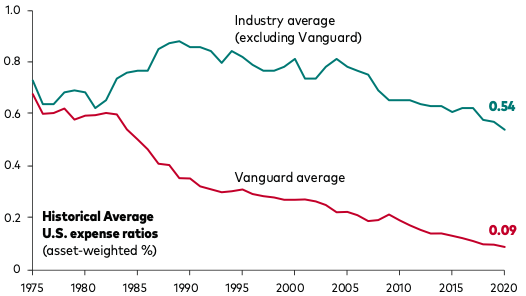

The cost of financial products is important, and Slack Investor does his best to minimise any fees that come with financial transactions. It is not often I get to talk about two of my favourite finance things in one blog. Vanguard, the low-cost fund trendsetter and superannuation.

Vanguard have long been a fund manager and ETF provider that have been at the forefront of lower fees in the finance sector. The term “Vanguard Effect” has been coined to explain the phenomena that when Vanguard competes in an area, the expense ratios from their competitors tend to decrease.

Tracking the average Management Expense Ratio (MER) for US Index funds – Vanguard

Vanguard Superannuation in Australia

This month, Vanguard launched into the Australian Superannuation space with a product that is transparent and amongst the lowest fees for an accumulation account. The beauty of their offering is the straight up bundling of all their fees into one simple number – 0.58% of your super balance. Of course, Slack Investor would like a lower management fee – but this is a good start.

The Vanguard MySuper Lifecycle product fees depend on how much Super you have. For a $50,000 balance, the total annual fee would be $290, for a $500,000 balance, the total annual fee would be $2900. The transparency is good – Drag out your own Super annual statement and try to work out your own total fees.

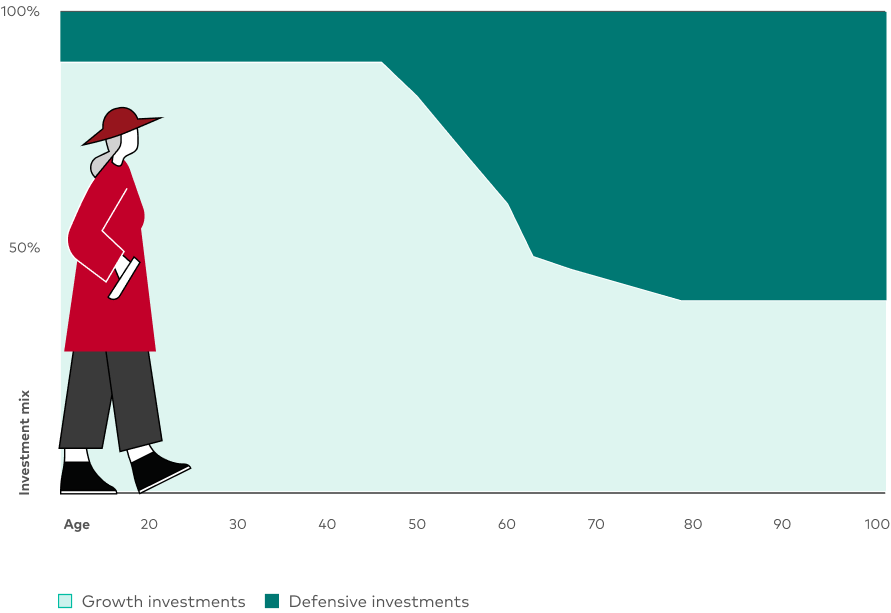

Of course, fees are not the only consideration. Many of the Industry funds use some sort of stock picking, and may use private equity to enhance their performance. Vanguard Super is made up of a mixture of index funds. I do like the way that the Vanguard Lifecycle automatically adjusts your exposure to risk as you creep towards retirement. 90% growth assets till age 45, then tapering to below 50% when you reach 60. All this is done automatically by Vanguard.

The adjustment of exposure of the Vanguard Livecycle super between growth and defensive assets as you age – Vanguard

Despite this juicy offering, there is often a lack of engagement of Australian workers with their superannuation. Vanguard will probably have a bit of trouble gaining traction in Australia due to the size and popularity of their industry super competitors. This product is currently only for accumulation accounts at this stage. It is a decent starting point by Vanguard and l0ok forward to details of their pension option (coming soon!). I also am hopeful of a bit of the “Vanguard Effect” to put a bit of pressure on existing superannuation fees – which are still too high.

A note that Slack Investor is not sponsored by Vanguard (or anyone else!), but I own a few of their ETF’s and their original founder, Jack Bogle, is one of the Slack Heroes.

November 2022 – End of Month Update

Slack Investor is now back IN for Australian index shares, UK Index shares and UK Index shares.

Last month’s update describes why I feel glad that my 20-yr index timing experiment is coming to an end in 2024. The frustrating moving out … then quickly back in to my Index funds is getting tiresome. I am likely to become just a “buy and hold” investor for my small portfolio of Index funds.

This month, all markets found there were “Reasons to be Cheerful”. There were positive movements all round. The ASX 200 +6.1%, the FTSE 100 +3.3% and the S&P 500 +5.4%.

All Index pages and charts have been updated to reflect the monthly changes – (ASX Index, UK Index, US Index).

I am hoping that your retirement does not upset as many people as in this James Gillray (1756-1815) painting of “Integrity Retiring From Office”. You can hopefully avoid this by leading a good life and providing yourself with income for this wonderful stage of your life.

There are lots of ways to do this – Slack Investor likes to separate his non-house assets into a Stable Pile and an Investment Pile in his Self Managed Super Fund (SMSF). Most of the commentary on this website has been about the Investment pile as this is the most exciting – and produces the most gains – and lately, the most losses. My Investment pile is volatile as there is greater risk (and opportunity for growth) in this part of the portfolio.

The Stable Pile is mostly to supply me with guaranteed income during the market downturns. Slack Investor’s Stable pile consists of Cash, Term Deposits, An Annuity, Fixed Interest, Real Estate and Bond ETF’s, and some dividend-producing consumer-staple shares.

If the previous financial year has been a good year for investments, my next years annual income requirements can be withdrawn from the investments pile. If you get a bad year for investments, then, I dip into the stable income pile. I try to keep my ratio of Investment Pile to Stable Pile at about 70%:30% and I roughly rebalance at about this time of year (July/August/September).

Using this method, you are always selling from your investments pile when the market is high and buying when the market is low

This method suits Slack Investor, but there are other ways to provide yourself with income in retirement.

Dividends

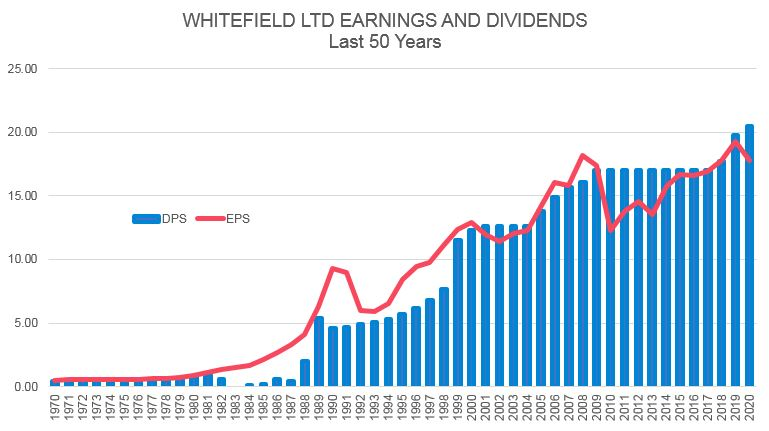

The well known Australian investor Peter Thornhill, is a great proponent of using dividends to provide retirement income. His MySay articles are well worth a read. Peter maintains that dividends supply an inflation-protected, income that doesn’t vary as much as stock prices do. He supports this strategy by keeping sufficient cash in his superannuation account to fund the next 3 years minimum pension withdrawals (For the Australian superannuation system) – this helps avoid forced selling. The rest of his fund is in Industrials and Listed Investment Companies (e.g. Argo (ARG), Whitefield (WHF)). He has tested his strategy through market cycles and his strategy has been vindicated through the Covid-19 downturn with even some LIC’s using maintained profits to keep dividends going.

Whitefield Ltd is a Listed Investment Company (LIC) that has generally maintained its dividend Per Share (DPS – blue columns) for the past 50 years – even during periods of downturns where the Earnings Per Share (EPS – Red line) of its contributing companies were declining. From Peter Thornhill

Lifetime Annuity Payments

There are many different types of annuity. Annuities have not been very popular in Australia due to their pricing, relative complexity and inflexibility. Challenger has a few of these products available in Australia with rates at September 2022 for a lifetime inflation-protected annuity of $5104 for a 65-yr-old male for every $100000 invested. There are other options for payments that can be either deferred or market linked. Although you can access these annuities directly through their website, the current model that Challenger prefers is access through a financial advisor.

Retirement Income Stream products

Way back in the Australian 2016/17 government budget, Treasury proposed a series of reforms that included removing barriers to innovation in retirement income stream products. This tinkering was brought about by the realisation that the Australian Super model was mostly fit for purpose in the “accumulation” stage – but was lacking in retirement income stream products that address Longevity Risk – the risk of outliving your savings.

Hopefully, with the benefit of compulsory superannuation, most people would have a pile of superannuation money when they retire – and a desire to turn that pile into income (after paying off any debts). Everybody wants to maintain their standard of living in retirement and would prefer something to invest in that would give them the peace of mind of having a guaranteed income stream for life.

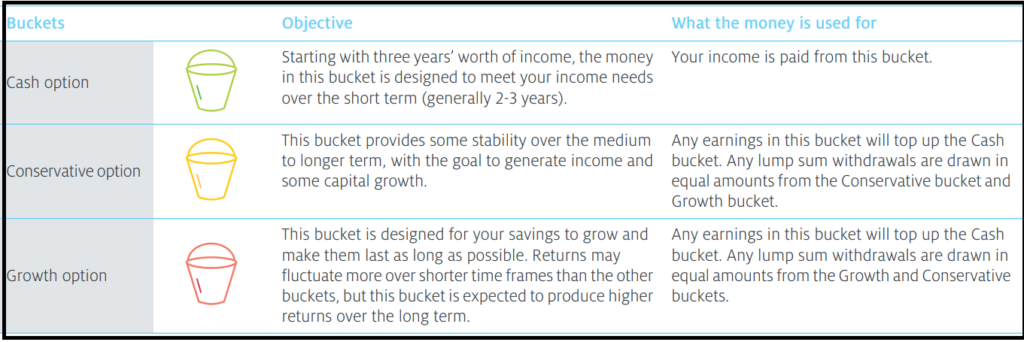

At last some new products are staring to emerge from the super funds. Slack Investor was excited to come across the MyPension income stream from Equipsuper. It is a “set-and-forget” investment strategy that nicely mixes a bit of risk assets (to keep your pension fund growing) with more conservative elements (to maintain a more steady income). This fund uses a similar method to the Slack Investor strategy of using “piles” or “buckets”.

To use the Equip MyPension, you would have to roll your existing super into their fund on retirement. Your super is separated into three distinct investment ‘buckets’. The automatic rebalancing of this product would suit those who want to be a bit more “hands off”.

Equip MyPension option for maintaining a retirement income stream.

Cash – For regular income payments, usually comprised of three years income – about 20% of investment.

Conservative – Investments in low risk categories including cash and bonds – about 40% of investment.

Growth – Investments to grow your savings, subject to short term fluctuations – about 40% of investment.

The clever thing is how these buckets work together over time. When investment markets are good, any earnings in the conservative and growth buckets go into the cash bucket, locking in your gains (Automatically). If markets experience a downturn, we’ll leave any buckets that lose value untouched at the end of year, to allow them to recoup losses in future years.

Slack investor has just two piles for his retirement – the Stable Income pile (Cash and Conservative) option and an Investments pile- and I do my own annual rebalancing. My investment pile is a bit more aggressive than the EquipSuper offering – more volatile, but Slack Investor likes to meddle and, is developing a “strong stomach”.

Like Sally, one day the realization will come that your best interests rely on you steering your own bike – in the direction that you want to go!

The ultimate goal is to get your three substantial piles going – house, income and investments. But before any of this happens you have to develop a mindset … I want to be in control of my financial life.

You must gain control over your money or the lack of it will forever control you. —

If you don’t take control, perhaps you’re plan is to take all your affairs to a financial adviser one day. Most people will feel the need for financial advice at some stage but only 20% of Australians have a financial advisor. The current structure makes getting advice a difficult step – and it’s not the financial advisors fault.

The pricing problem of Financial Advice in Australia

64% of survey participants agreed that financial advisers were too expensive.

The Australian Government passed a piece of legislation known as the Future of Financial Advice (FoFA) in 2012. FoFA was a series of laws that were supposed to improve the quality and transparency of financial advice. One of the main purposes was banning conflicted remuneration – where advisers were recommending products that gave them good commissions. While FoFA and the Hayne Royal Commission were well intended and vital in restoring some trust in the sector – there have been some unintended consequences.

(The Financial Services Royal Commission) identified the problem of conflicted remuneration without providing a mass market solution.

There has been a huge rise in regulatory red tape and the associated compliance costs for financial planners. A combination of these costs, the big banks dumping their financial advice arms, and the need for upgraded qualifications has put this sector in crisis. The total number of licenced advisers is set to drop by a third in the next few years.

There is broad recognition that financial advisors have expertise that the normal punter does not have. However, the biggest barrier to getting financial advice is the expense. One of the big problems is that when you engage a financial advisor, they are obligated to present you with a full Statement of Advice (SOA). On the surface this makes sense, the client would want a document that takes into account your own circumstances and outlines the fees and risks of each strategy. However, according to one planner, the SOA has turned into pages of jargon, repeated disclosure and boring generic graphs. These statements are weighty tomes that take many hours to prepare. Sadly, they seem to confuse the actual adviceand provide no real value to the client.

A full Statement of Advice (SOA) runs over 100 pages and the need to review all circumstances and develop a plan takes 10 to 15 hours and costs between $3,000 and $5,000 depending on complexity.

James Kirby from The Australian uses the example of paying annual adviser fees fees of $3000 and he supposes that the structured advice that you receive will match the 4.3% pa return of the new Magellan retirement income product Magellan FuturePay (FPAY). He points out that for an investment of $500 000 and an expected FPAY return of $21 500, your advice fees would be 14% of your earnings. This does not make sense to him … or Slack Investor.

James Kirby suggests that a better model for the regulators to adopt would be that you could approach a financial adviser for advice that you need at the time … and pay the financial adviser for this “niche” advice. This is not possible under current legislation.

Take charge

So, with full service financial advice gravitating towards high net wealth clients, what is the average punter supposed to do? Robo-advisors such as Stockspot could be part of the solution. This automated service can provide help with allocation of assets other services that will suit your age and risk profile. But there are so many more financial questions you might want to handball to your financial adviser if you could afford one. Well, if you can’t … it’s up to you.

Decide what you want to achieve in the finance sense. Go through the savings basics and get your savings rate up. Take charge on where your money goes, get your superannuation set, reduce any unnecessary fees that you are paying, set a target on your financial piles.

Educate yourself on things financial. There are some great books. The Barefoot Investor is an excellent start. Some fabulous podcasts The Australian Finance Podcast will get you going and there are heaps of other Slack Investor favourites. Get involved and start to enjoy the immense freedom and satisfaction of riding your own bike.

Happiness is not in the mere possession of money; it lies in the joy of achievement, in the thrill of creative effort.